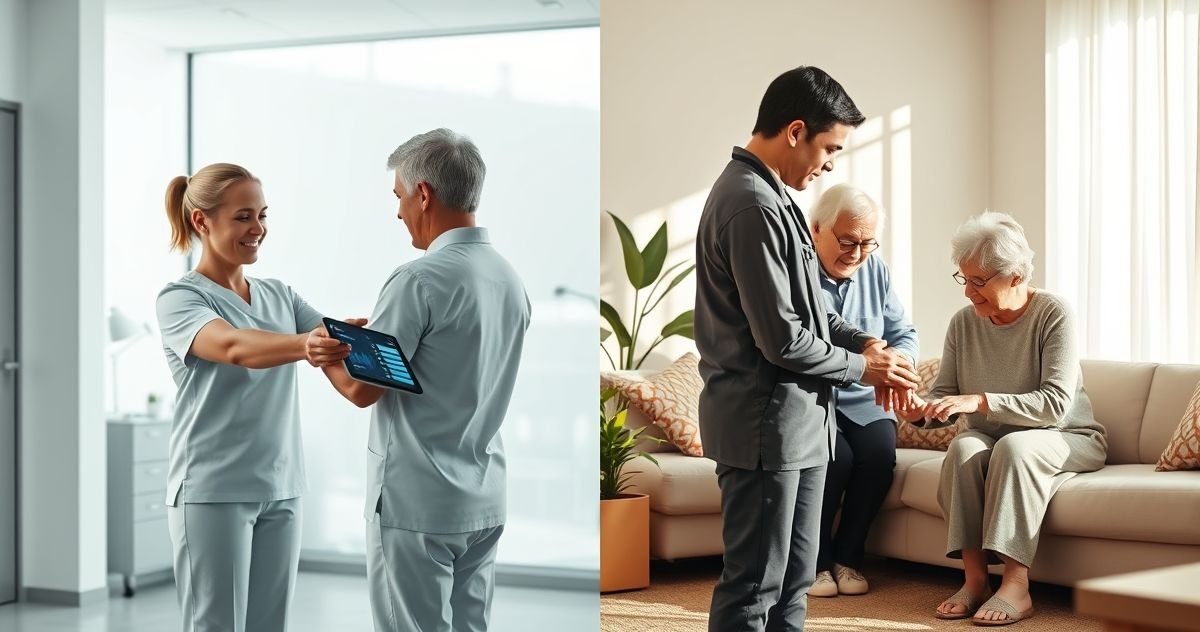

Overview

Choosing between short-term and long-term care options is a practical decision that affects your medical recovery, independence, and financial security. Short-term care typically supports recovery from surgery, injury, or a brief illness. Long-term care provides ongoing help with activities of daily living (ADLs) — such as bathing, dressing, eating, and medication management — when a condition becomes chronic or progressive.

Why the distinction matters

- Payer differences: Short-term care is often covered by Medicare or private health insurance when it’s medically necessary; long-term care usually is not covered by standard health plans and requires separate strategies. (Centers for Medicare & Medicaid Services — CMS)

- Duration and goals: Short-term care is time-limited and goal-oriented (rehabilitation); long-term care is focused on sustained support and quality of life.

- Cost and setting: Long-term care is commonly more expensive over time and more likely to be delivered at home, in assisted living, or in nursing facilities.

How short-term care works

Short-term care is designed to restore a patient’s health and independence after an acute event. Typical settings include:

- Hospital inpatient recovery

- Skilled nursing or rehabilitation facilities (following a qualifying hospital stay)

- Home health care for short periods (skilled nursing or therapy)

What Medicare covers: Medicare Part A may cover skilled nursing facility (SNF) care up to 100 days after a qualifying 3-day hospital stay when skilled care is needed for recovery. Coverage rules are specific about medical necessity and documentation; verify eligibility with CMS and your provider. (CMS: https://www.cms.gov)

In my practice I’ve seen clients avoid large rehab bills by documenting therapy needs carefully and using the Medicare SNF benefit after surgery—this can substantially reduce out-of-pocket costs for a defined recovery period.

How long-term care works

Long-term care supports people who need help with ADLs or have cognitive impairment (like Alzheimer’s) for months or years. Settings include:

- In-home caregivers or home health aides

- Assisted living communities

- Memory care or specialized long-term care facilities

- Nursing homes for higher medical needs

Long-term care often requires a funding plan: private long-term care insurance, hybrid life/LTC products, self-funding from savings, or Medicaid for those who meet eligibility rules. Medicaid eligibility and benefits vary by state and typically require financial planning (for example, understanding look-back periods). (National Institute on Aging: https://www.nia.nih.gov; CMS: https://www.cms.gov)

Coverage and payment: what to expect

- Medicare (short-term focus): Covers medically necessary skilled care for a limited time. It is not a payer for most custodial long-term care needs.

- Private health insurance: May pay for medically required rehab or home health services, but usually excludes long-term custodial care.

- Long-term care insurance: Pays for custodial services (based on policy triggers). Policies vary widely in daily benefit, elimination period, inflation protection, and benefit period. See our glossary on long-term care insurance for details: Long-Term Care Insurance.

- Medicaid: Pays for long-term services for eligible low-income people; rules differ by state and often require planning to qualify without exhausting assets. See our guide on Medicaid planning: Medicaid Lookback and Long-Term Care Planning Explained.

- Hybrid products and other strategies: Hybrid life/LTC policies or riders can provide death benefit protection with LTC access; annuities with LTC riders are another option. For a funding comparison, read our article: Evaluating Long-Term Care Funding Options: Insurance vs Self-Funding.

Typical costs and ranges (planning guidance)

Costs vary by location, level of care, and setting. Use these as planning estimates, not guarantees:

- Short-term inpatient rehab or SNF: Covered partially by Medicare for eligible stays; private pay for extended rehab may be thousands per week depending on services.

- In-home care: Part-time home health aides or personal care can range from tens of dollars per hour; full-time home care can exceed $40,000–$100,000 per year depending on hours.

- Assisted living: Varies widely — often $30,000–$70,000 per year regionally.

- Nursing homes (long-term residential care): Can exceed $100,000 per year for a private room in higher-cost regions.

(For national comparisons and latest surveys, see the NIA and state Medicaid resources: https://www.nia.nih.gov, https://www.cms.gov.)

Common real-world examples

- Post-surgical rehab: A patient discharged after hip replacement uses home health physical therapy for 4–6 weeks; Medicare covers skilled nursing or therapy when criteria are met. This is short-term, recovery-focused care.

- Progressive care: A person with dementia who needs daily supervision and help with ADLs requires long-term assistance. Family caregivers often supplement paid help until a move to assisted living or memory care is needed.

Decision checklist: which option do you need?

- Define the goal: recovery with measurable therapy gains (short-term) or ongoing daily help (long-term).

- Assess function: use ADLs (bathing, dressing, eating, toileting, transferring, continence) and IADLs (meal prep, medication management, transportation) to determine level of support needed.

- Review payer rules: check Medicare eligibility for SNF benefits, home health coverage, and private insurance terms.

- Estimate costs: get local quotes for home care, assisted living, and nursing facilities.

- Consider funding: evaluate LTC insurance, hybrid products, or savings; plan for inflation and care escalation.

- Legal & care planning: durable power of attorney, advance directives, and a care preferences document.

Planning strategies and professional tips

- Start early: I encourage clients in their 50s and early 60s to review long-term care options and to get insurance quotes or create a savings approach before premiums rise or health conditions emerge.

- Use hybrid policies selectively: Hybrid life/LTC products can protect legacy goals while covering care needs; compare total cost and scenarios.

- Leverage tax-advantaged accounts: Health Savings Accounts (HSAs) can supplement short-term and some long-term costs — read our piece on using HSAs to supplement retirement healthcare costs: Using HSAs to Supplement Retirement Healthcare Costs.

- Document medical necessity: For Medicare SNF benefits, clear documentation and timely appeals can make coverage decisions favorable.

- Plan for inflation: Include 3–5%+ annual increases in care costs in long-term projections.

Common mistakes to avoid

- Assuming short-term coverage covers chronic needs: Medicare and many private plans limit coverage to recovery-related skilled care.

- Waiting too long to plan: Health changes can disqualify you from insurance or make premiums unaffordable.

- Overlooking informal care costs: Family caregiving has real costs — lost wages, stress, and potential need for paid support.

Frequently asked questions

Q: Can Medicare pay for long-term care in a nursing home?

A: Medicare covers skilled nursing facility care for a limited, medically necessary period after a qualifying hospital stay; it does not cover custodial long-term care for ongoing ADL assistance. (CMS)

Q: When should I buy long-term care insurance?

A: The “best” time balances premium affordability and health status—commonly in the late 50s to early 60s for many buyers. Get quotes and review riders, inflation protection, and elimination periods.

Q: Is Medicaid the only option for very high long-term care costs?

A: Medicaid is a major payer for long-term services for those who meet income and asset limits, but planning (including trusts and spend-down strategies) is often needed and should be done with counsel. (CMS, state Medicaid offices)

Professional disclaimer

This article is educational and reflects professional experience in financial planning. It does not replace personalized medical, legal, or tax advice. Consult a certified financial planner, elder law attorney, or your healthcare provider to design a plan that fits your situation.

Authoritative sources and further reading

- Centers for Medicare & Medicaid Services (CMS): https://www.cms.gov

- National Institute on Aging (NIA): https://www.nia.nih.gov

- Consumer Financial Protection Bureau: https://www.consumerfinance.gov

Related FinHelp guides

- Evaluating Long-Term Care Funding Options: Insurance vs Self-Funding — https://finhelp.io/glossary/evaluating-long-term-care-funding-options-insurance-vs-self-funding/

- Long-Term Care Planning and Funding Options — https://finhelp.io/glossary/long-term-care-planning-and-funding-options/

- Using HSAs to Supplement Retirement Healthcare Costs — https://finhelp.io/glossary/using-hsas-to-supplement-retirement-healthcare-costs/